.png)

Behavioural Coaching

Is It Safe to Invest Right Now? This Is What Smart Investors Are Doing

Is it safe to invest right now? A Canadian planner walks through the data on market drops, all-time highs, and what smart investors actually do.

May 13, 2026

Table of Contents

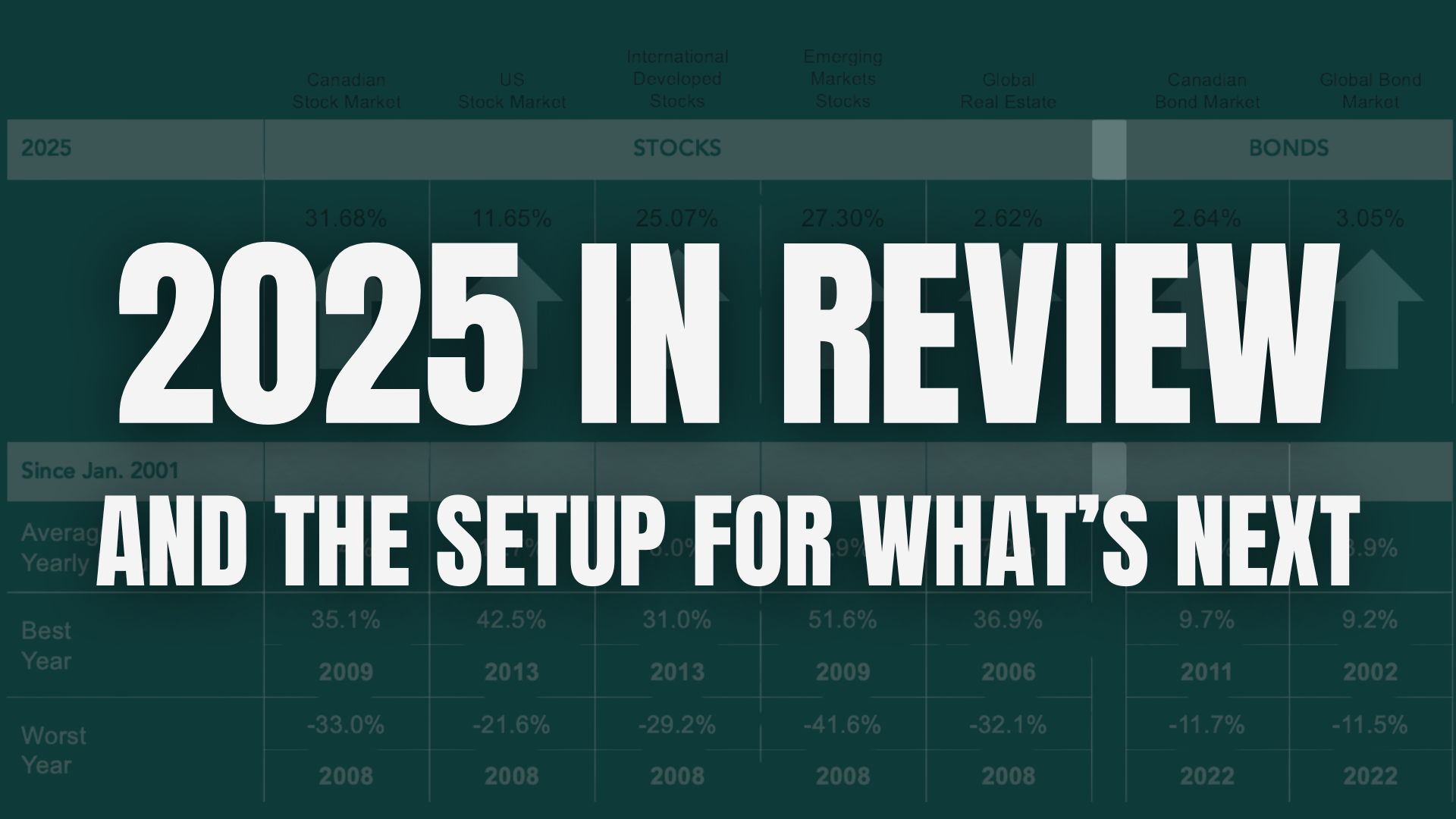

TL;DR. When the stock market drops, most people want to sell. The data says don't. Selling locks in your loss. Then you have to guess when to buy back in — and most people guess wrong. In 2025, more than 93 out of every 100 Canadian stock funds did worse than just owning the whole market. And if you're scared because stocks are at a record high, that isn't a warning sign either.

The simple things to do when the market is wild: fix your investing mix back to your plan, use losses to lower your taxes, and look at your big plan — not your account balance.

Eight different clients have asked me some version of the same question lately:

- "Should I be selling?"

- "Should we put less of our money in stocks?"

- "Should we wait to do the renovation until things calm down?"

The answer was no every time. Let me show you why — the reason is almost always the same.

Should I sell when the stock market is going down?

When you sell while stocks are falling, two bad things happen at the same time.

First, you turn a paper loss into a real one. If you don't sell, your account just looks lower for a while. The moment you sell, the loss is locked in. It's real.

Second, you now have to make another tough choice — when to buy back in. Most people don't get that one right either. They wait until things "feel safe." Usually by then, most of the bounce-back is already over.

Dimensional looked at this with a simple test. Imagine you put $1,000 into a big basket of U.S. stocks in 1998, and held until the end of 2022:

- Stayed in the whole time: $6,356

- Missed the best 1 week: $5,304

- Missed the best 3 months: $4,480

Missing only the best 3 months over those 24 years cut the final account value by about 30%.

Why? The best days for stocks almost always happen during the scary times. The days you most want to be out are right next to the days you most need to be in. Nobody has found a way to tell them apart ahead of time.

How often does the stock market actually go down?

It feels scary in the moment. But the truth is, it happens all the time. Here is what the U.S. stock market did each year from 1979 on:

- Average drop within a single year: about 14%

- Years with a drop bigger than 10%: about half

- Years with a drop bigger than 15%: about a third

- Years that still ended up with a gain: 34 of 41

So even with all those scary drops, most years finished up.

Zoom out further and it gets clearer. The only times U.S. stocks have actually lost money over a full 10 years were during the worst events of the last 100 years: the Great Depression, the Tech Bubble, and the 2008 Financial Crisis. You basically need a once-in-a-generation crash to lose money over a whole decade in U.S. stocks.

If you have only been investing for a few years, this might be your first big drop. That doesn't make it different. It just makes it new to you.

How much does panicking cost the average investor?

Morningstar runs an annual study called Mind the Gap. It checks two numbers — and they are not the same.

People buy after stocks have already gone up. They sell after they have gone down. That hurts their returns.

Looking at the 10 years through the end of 2024:

- What the funds returned: 8.2% per year

- What the average investor earned: 7.0% per year

- The gap: 1.2% per year — the cost of reacting

That 1.2% per year is not fees. It's just the cost of reacting. Over a whole career, the gap is bigger than most of the fee discussions people get worked up about.

Can a great fund manager keep me safe in a crash?

This is the other thing people ask. The data is not on the side of the fund manager.

SPIVA Canada — 2025 calendar year:

- Canadian Equity funds that did worse than the market: 93.4%

- Canadian Focused Equity funds that did worse: 93.1%

- Canadian Small / Mid-Cap funds that did worse: 100%

SPIVA U.S. — 15 years through end of 2024:

- Fund categories where most managers beat the market: 0 of 22

- Big U.S. stock funds that did worse than the S&P 500: over 90%

Paying a fund manager to "dodge the drops" is a plan that has failed more than 9 out of 10 times. That isn't really a plan.

Is it safe to buy stocks at a record high?

This is the flip side of "should I sell?" — same fear, different shape.

Dimensional says it plainly in their guide for everyday investors:

Buying shares at all-time records has, on average, produced similar returns to stocks bought following a sharp decline. This suggests that trying to time when to get into and out of markets is unlikely to lead to better results.

— Dimensional Fund Advisors

Stocks hit new highs all the time. It is part of how they grow over the long run. A new high is not a warning that a crash is coming. Sitting in cash waiting for a "better" time to buy isn't safer than just buying. On average, waiting just costs you the money you would have made.

Should I move my money out of the U.S. because of trade fights and politics?

When clients ask me this, my answer is usually: a good plan is already taking care of that.

A good portfolio owns a little bit of everything — U.S. stocks, Canadian stocks, stocks from other countries, and bonds. When one part drops, another part usually holds up. You don't have to guess which one will do well.

The mistake is trying to outsmart it. You sell the part that scared you. Then the scary news doesn't matter the way you thought it would. And now you missed the bounce back. You made a bet — and the data says you probably won't win it.

What you should actually do when the market gets scary

Four things. None of them are "sell everything."

01. Look at your plan, not your balance.

If you don't need this money for 30 years, a 15% drop is not a problem. If you're about to retire, we may want a more balanced approach to limit exposure to the volatility. Time horizon is the variable that actually matters.

02. Fix your investing mix back to your plan.

When stocks drop, you end up with less of your money in stocks than your plan called for. The right move is to sell a little bit of bonds and buy more stocks. It feels scary — which is exactly why most people don't do it.

03. Use losses to lower your taxes.

In a regular (non-registered) account, if something you own is worth less than what you paid, you can sell it and use that loss to lower your future tax bill. A bad year turns into a tax win — TFSA & RRSP don't count.

04. Stress-test the plan, not your nerves.

Run the numbers and see what would have to happen for the plan to actually break. The answer is almost always: way worse than what's happening today. Once you see that on paper, the panic gets smaller.

FAQ

Should I sell when the stock market drops?

No, almost never. Selling locks in the loss and forces you to guess when to buy back in. Most people guess wrong. The best days for stocks tend to happen during the scariest weeks, so being out misses those days.

Is it bad to buy stocks at a record high?

No. Dimensional's research shows that buying at all-time records has, on average, made you about the same money as buying after a big drop. A new high doesn't mean a crash is coming.

Can my advisor protect me from a stock market crash?

Not the way most people imagine. SPIVA Canada shows that in 2025, 93.4% of Canadian Equity funds did worse than the market, and 100% of small and mid-size company funds did worse. What a good advisor actually does is keep you invested when it's scary, fix your mix back to plan, and use losses to save you tax.

What is the "behaviour gap" and why should I care?

It's the gap between how funds do and how much real people in those funds actually earn. Morningstar says it's about 1.2% per year, and over a whole career that adds up to a lot of money. It happens because people buy high and sell low.

Should I sell my U.S. stocks because of trade fights?

A good global portfolio already owns stocks from many countries. You don't need to guess which one will win this year. The mistake is making bets on top of a portfolio that's already doing the work for you.

The big lessons

- Selling when the market drops locks in your loss and forces a second hard choice most people get wrong.

- Most of the best days for stocks happen during the worst weeks. Missing a few wrecks your long-term result.

- Most fund managers don't beat the market — in 2025, 93.4% of Canadian Equity funds did worse.

- The behaviour gap costs about 1.2% per year — bigger than most of the fees people argue about.

- Record highs are not dangerous. On average, buying at a record has done about as well as buying after a drop.

- Fix your mix. Use losses to save tax. Look at your plan, not your account.

If you want a second set of eyes

Want someone to look at your plan with you before the next big drop? At Millen Wealth we help Canadian young families, tech workers, and small business owners build clear plans for their money.

Sources

- Dimensional — What Happens When You Fail at Market Timing

- Dimensional — Recent Market Volatility

- Morningstar — Mind the Gap 2025 (landing page) · full PDF

- S&P Dow Jones Indices — SPIVA Canada Year-End 2025

- S&P Dow Jones Indices — SPIVA U.S. (landing page) · Mid-Year 2025 PDF

- Dimensional — What Every Investor Should Know

- Winthrop Wealth — How has the S&P 500 historically performed over 10-year periods?

- Dimensional — In Shaky Times, Investors Should Hold Their Nerve

Disclaimer. Past performance is not a guarantee of future results. The data and research cited above are provided for educational purposes and do not constitute investment advice. Individual circumstances vary; consult a licensed financial planner before making investment decisions.